The narrative around DeFi post-October 10th is shaping up to be a bit too simplistic. We're seeing headlines about a "crash" and broad sector weakness, but diving into the numbers reveals a more nuanced picture – one where specific sub-sectors are not only surviving but potentially thriving. It's not a uniform disaster, it's a reshuffling of the deck.

DeFi: A Flight to Perceived Safety (and Maybe Illusion?)

The DeFi Dichotomy: Beyond the Headlines

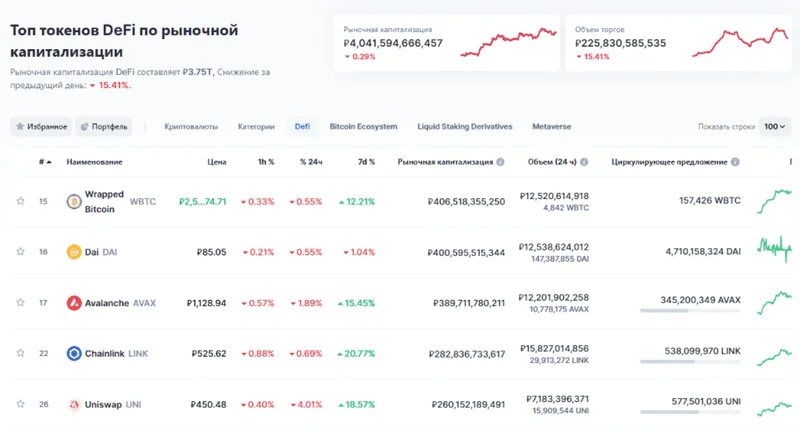

FalconX's report highlights that only 2 out of 23 leading DeFi tokens are positive YTD as of November 20th, and the group is down 37% QTD. That paints a grim picture, no doubt. But averages can be deceiving. What's really happening under the surface?

Investors appear to be rotating into perceived "safer" names – those with buyback programs (like HYPE and CAKE) or those with idiosyncratic catalysts (MORPHO and SYRUP). This suggests a flight to quality, or at least a flight to *something* tangible, within the DeFi space. Are buybacks really a sign of strength, or just financial engineering propping up otherwise weak tokens? It's a question worth asking. What happens when the buybacks stop?

And then there's the shifting valuation landscape. Spot and perpetual DEXes have seen declining price-to-sales multiples. But some DEXes, like CRV, RUNE, and CAKE, actually *increased* their 30-day fees between September 30th and November 20th. So, while the market is punishing DEXes broadly, actual usage hasn't necessarily cratered across the board. It seems some DEXes are carving out a niche, maybe by offering something unique or simply by being better run.

Lending and yield names present another puzzle. Their multiples have broadly *steepened* because prices haven't declined as much as fees. One example: KMNO's market cap fell 13%, while fees declined 34%. Investors might be crowding into lending names, viewing them as more resilient during the downturn. But is this a rational assessment, or just a herd mentality? Are they overestimating the stickiness of lending activity?

"Best Crypto" Lists: Marketing Masquerading as Research?

Digging Into the "Best Crypto" Lists: A Grain of Salt Needed

Then we have the "best crypto to buy" lists popping up everywhere. Coinspeaker, for example, touts Bitcoin, Solana, and XRP as "established" choices, while pushing Ondo Finance and Immutable as "early stage" opportunities. Their methodology supposedly balances growth potential, tokenomics, utility, and price action. But let's be real: these lists are often marketing exercises disguised as research.

Take their assessment of Ondo Finance. They praise its partnerships with BlackRock and Goldman Sachs and its SEC-compliant infrastructure. Fair enough. But then they casually mention that ONDO's price has declined significantly from its all-time high (down 63%!). And this is the part of the report that I find genuinely puzzling. How can you call something a "best crypto to buy" when its tokenomics are clearly a problem, as they themselves acknowledge?

Hyperliquid (HYPE) gets similar treatment. Coinspeaker highlights its high trading volume and no-gas-fee trading. All true. But they also mention a massive token unlock of $12 billion over 24 months. My analysis suggests that buybacks can only offset about 17% of that sell pressure. So, while the fundamentals might be strong, the tokenomics create a huge overhang.

And consider Zcash (ZEC). Coinspeaker touts its 560% rally and Grayscale Trust launch. But the RSI is screaming overbought. Plus, the EU's potential ban on privacy coins looms. It looks like a momentum trade, not a long-term investment.

These "best crypto" lists often overemphasize the positive while glossing over significant risks. They're useful as a starting point, maybe, but treat them with extreme skepticism. Especially since the coins that are being touted on these lists are the ones that are paying for advertising (parenthetical clarification).

CRO: A DeFi Microcosm – Hope vs. Harsh Reality

The CRO Story: A Microcosm of DeFi's Challenges

Cronos (CRO), the native token of the Cronos chain, offers a smaller-scale example of the broader DeFi trends. One analysis suggests it will reach a maximum of $0.1327 in 2025, with an average price of $0.1294. Optimistic, to say the least. An analysis of CRO's price can be found in

CRO price prediction 2025, 2026, 2027-2031.

Technical analysis paints a less rosy picture. On November 30, 2025, CRO traded near $0.1079, a slight dip from the previous day. The price remained confined to a narrow range, signaling limited volatility and no clear direction. Strong resistance capped upside attempts at $0.109, while key support held firm at $0.106. CRO is trading well below its all-time high of $0.9698 from November 2021 – to be more exact, the difference is 88.86%. That's a significant drop.

The token's value is tied to the performance of the Cronos Chain and the adoption of Crypto.com's products. While the project continues to develop and offer real-world utility, its price performance has been subdued. The analysts' sentiment is, on the whole, bearish.

One analysis says that CRO is likely to remain within its current tight range. A close above $0.109 would be the first sign of renewed bullish interest. But if buyers fail to reclaim that level, the price may continue drifting sideways. The $0.106 level remains the critical support to watch. A breakdown below this level could expose CRO to deeper weakness.

"Crash" is Too Simple a Word

The DeFi sector is not collapsing. It's evolving. Some projects are failing, others are adapting, and a few might even be thriving. The "October crash" narrative is a simplification that obscures the complex dynamics at play. Investors need to look beyond the headlines and dive into the data to understand what's *really* going on.

A Gut Check Needed

The data shows a clear divergence: some DeFi sectors are getting hammered, while others are attracting capital and user activity. The question isn't whether DeFi is dead, but where the real value is being created – and whether that value is sustainable or just a mirage.